While bond yields have risen sharply lately, fund flows into bonds tell two very different stories. We have previously written much on the recent rise in bond yields related to economic growth, event risks, and recessions. To wit:

“Since rates and expectations must adjust for the potential future impact on the current value of invested capital:

Equity investors expect that as economic growth and inflationary pressures increase, the value of invested capital will increase to compensate for higher costs.

Bond investors have a fixed rate of return. Therefore, the fixed return rate is tied to forward expectations. Otherwise, capital is damaged due to inflation and lost opportunity costs.

Therefore, the long-term correlation between rates, inflation, and economic growth is unsurprising.“

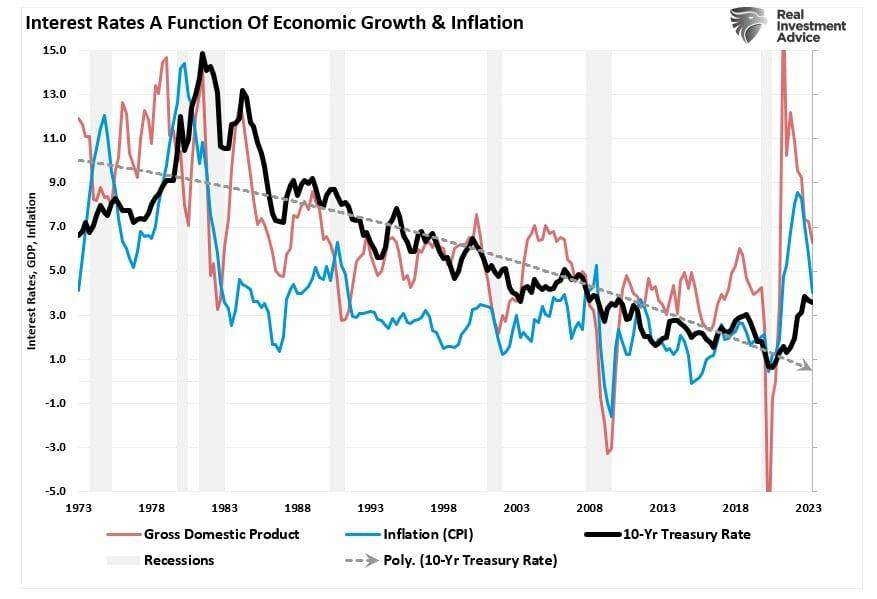

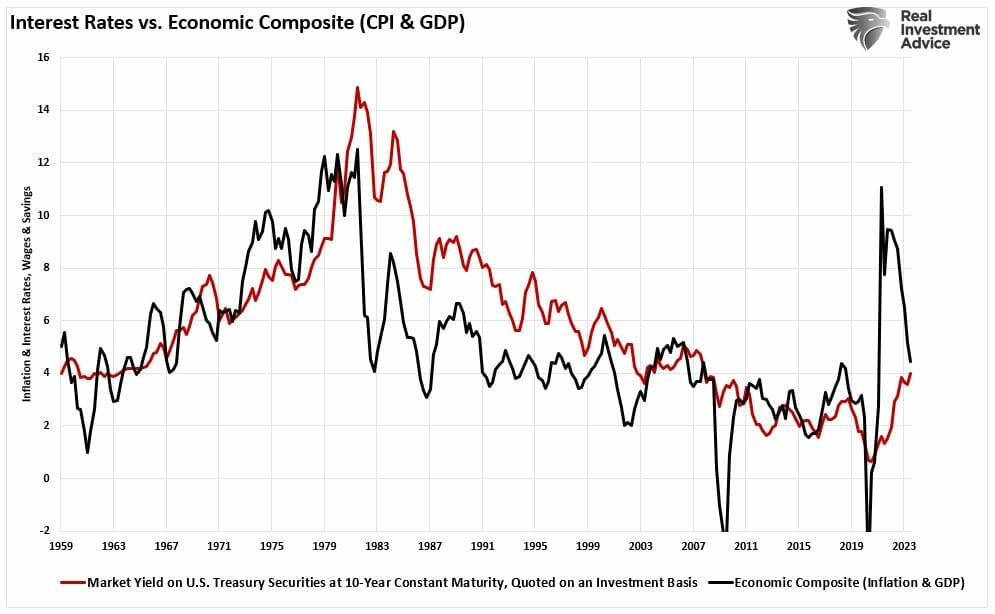

“That chart is pretty cluttered, so the following chart is a composite index of inflation and economic growth compared to the 10-year Treasury yield.”

Of course, that analysis contradicts the views of Ray Dalio, Bill Ackman, Bill Gross, and others who currently expect rates to go higher. The disconnect comes down to time frames. More importantly, investors must understand the difference between short-term market-driven narratives and the long-term economic dynamics that drive interest rates.

Such is the basis for our discussion in this blog.

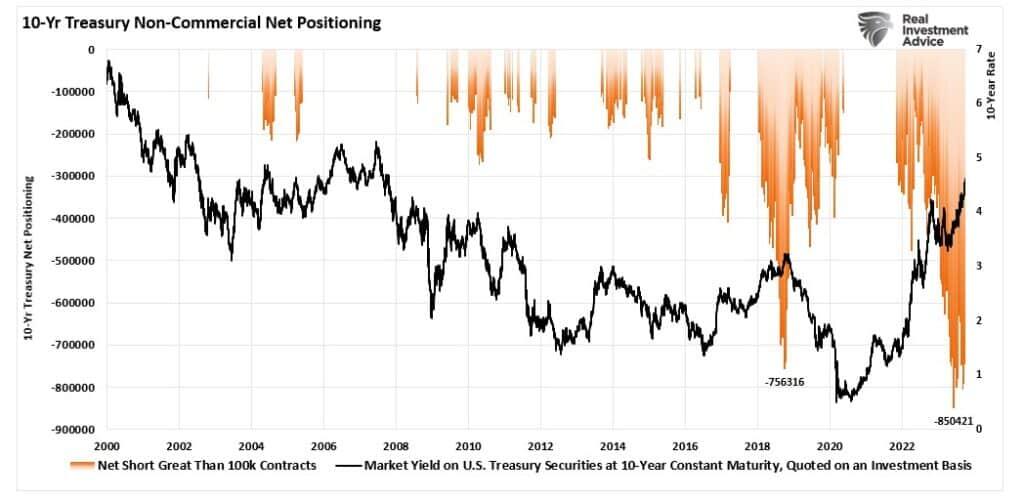

Traders Are Heavily Short Bonds

Over the last two years, interest rates on Treasury bonds have risen in response to two primary factors. On the short end of the Treasury curve, the 1-month to 2-year Treasury bonds are heavily influenced by the Federal Reserve’s monetary policy changes. As shown, there is an exceedingly high correlation between the Fed funds rate and the 2-year Treasury.

However, the long-end of the yield curve, 10-year Treasury bonds or longer, are driven almost entirely by expectations for economic growth, inflation, and wages, as shown above. Notably, the correlation is very high.

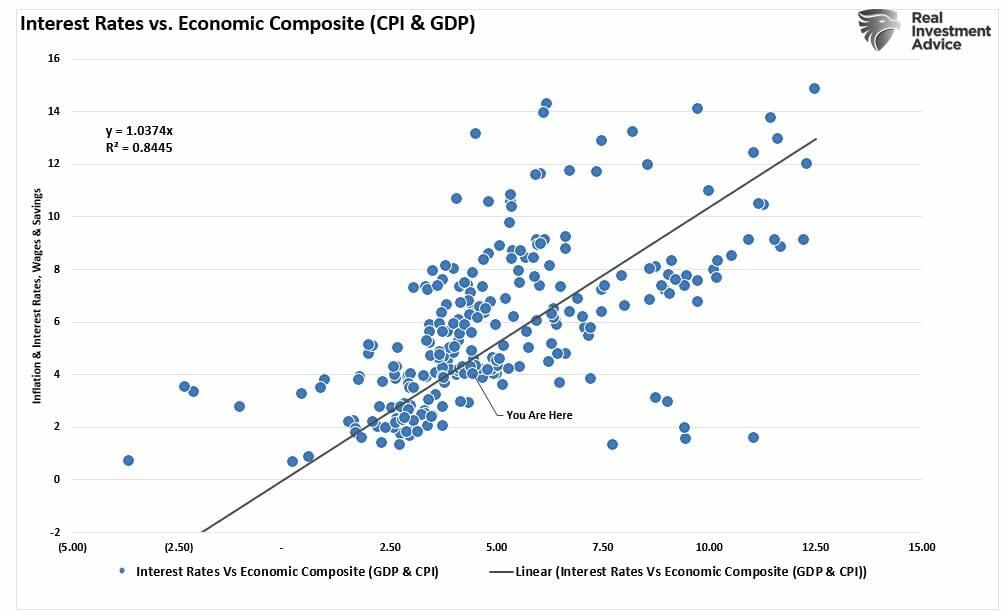

“As expected, the surge in economic growth and inflation pulled longer-duration yields higher. With a correlation of nearly 85% between interest rates and a GDP/Inflation composite index, investors should expect rates to fall as economic growth and inflation decline.”

Of course, there are periods where interest rates can, and do, diverge from the underlying economic fundamentals. We are experiencing one of those periods,driving the view that “rates must go higher.”

As we have discussed, the Commitment Of Traders (COT) report gives us some insights into what major fund managers, hedge funds, and commodity traders are doing. Given that yields on bonds are solely a function of the changes in price relative to its coupon, differences in yield can be influenced by market-driven actions in the short term.

The most recent COT report currently shows a record number of short positions against Treasury bonds. That “selling” pressure has pushed prices lower and yields higher, as shown below. We saw a similar episode during the “Taper Tantrum” in 2018.

Notably, when something “breaks,” those heavily “short” Treasury bond traders will be forced to cover those speculative positions. In 2018, the reversal of those speculative short positions on bonds was caused to cover as the Federal Reserve stepped in with a massive “reverse repo” program to bail out hedge funds.

As noted by TheStreet.com recently:

“It is clear that interest rates are driving the ship, but that ship could be on the cusp of taking a major turn.Maybe this time is different, but we doubt it. The odds favor an eventual unwind of the overly bearish 10-year note trade. The massive amount of short-covering could easily push yields back into the 2% handle.”

Of course, while rates rise and speculative traders short bonds, you might think no one is buying bonds.

However, you would be wrong.

Follow The Money

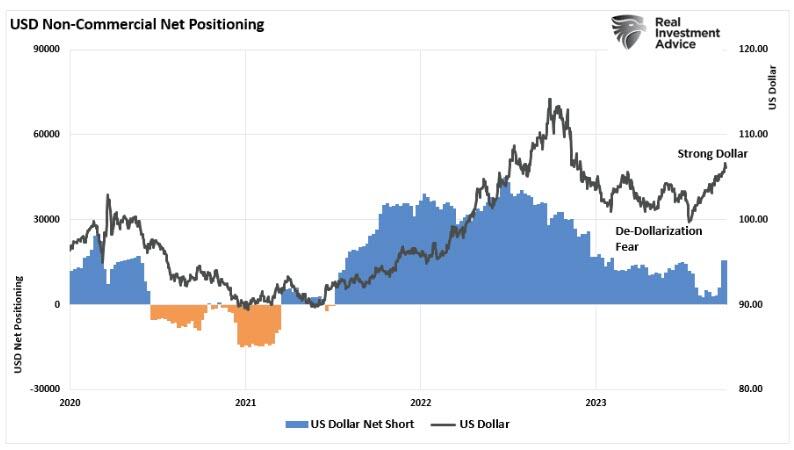

While speculators potentially drive higher yields in the short term, pay attention to fund flows. Two pieces of evidence suggest that rising yields aren’t a function of a lack of buyers. The first is the U.S. Dollar index.

Last year, there was a significant concern about a collapse in the U.S. dollar as “de-dollarization” would cause the loss of the reserve currency status. As both Michael Lebowitz and I discussed at the time, such would not be the case. To wit:

“Foreign nations accumulate and spend dollars through trade. They keep extra dollars to manage their economies and limit financial shocks. These dollars, known as excess reserves, are invested primarily in U.S.-denominated investments ranging from bank deposits to U.S. Treasury securities and a wide range of other financial securities. As the global economy expanded and more trade occurred, additional dollars were required. As a result, foreign dollar reserves grew and were lent back to the U.S. economy.“

This backdrop for the dollar is not changing anytime soon. According to the IMF, the dollar makes up almost 60% of global foreign exchange reserves. While the percentage has declined by about 10% over the last decade, it is still three times the next leading reserve, the Euro, which accounts for about 20% of global reserves. For those concerned about China, their currency, the renminbi (yuan), accounts for 2.5% of all reserves.

Not surprisingly, as the U.S. economy is more robust than its counterparts, and the yield on the 10-year Treasury bond is substantially higher, foreign excess reserves are now flowing into the U.S. Dollar.

When reserves flow into the U.S. dollar, those dollars are converted into U.S. Treasury Bonds. Such is why inflows into Treasuries continue to grow despite traders’ record short-position in Treasury bonds. As shown, the volume of fund flows into bonds is the highest since the 2020 economic shutdown.

While interest rates have stayed elevated, investors have turned to longer-term funds. As noted by Morning Star:

“Long-government funds were the most popular taxable bond category last year, during which time they hauled in $46.4 billion.“

For investors, the current rise in yields has undoubtedly been concerning. That rise, coinciding with much media spin about the “death of the dollar” and “debts and deficits,” certainly fueled the fears of spiraling interest rates.

However, when we “follow the money,” the fund flows suggest a different outcome.

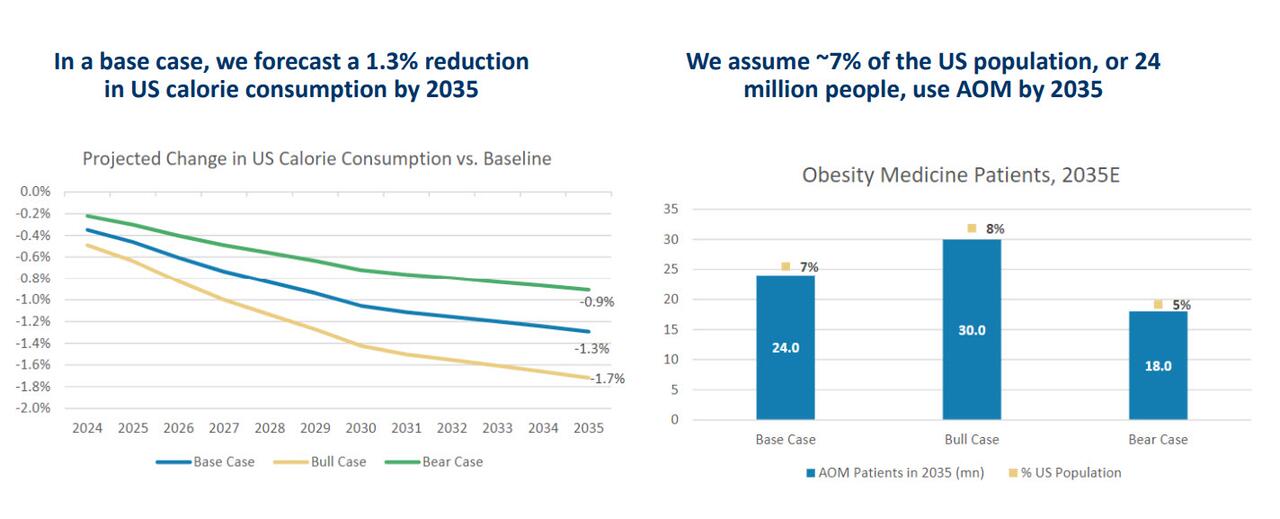

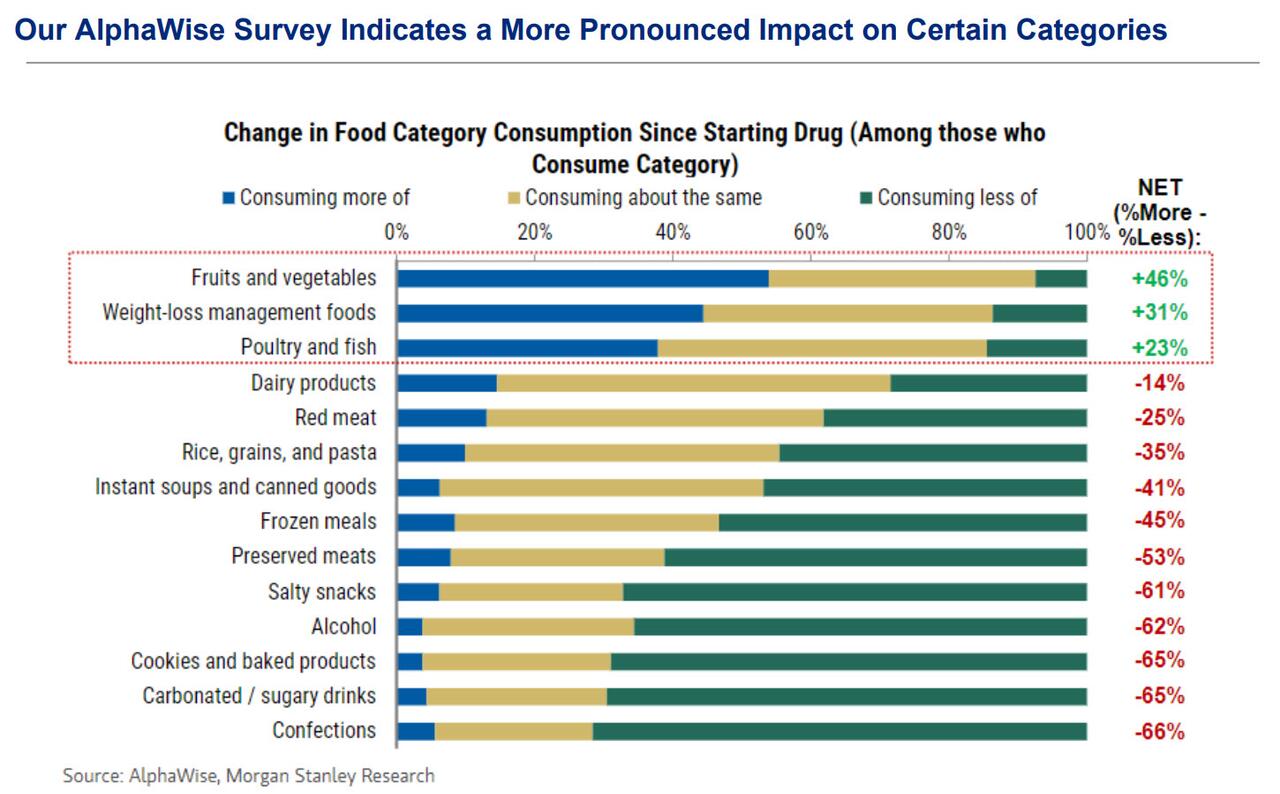

America's anti-obesity craze, courtesy of GLP-1-based weight-loss drugs such as Wegovy and Mounjaro, produced by Novo Nordisk and Eli Lilly, is in the early innings of unleashing a "food revolution" that could spark devastating consequences for the junk-food industrial complex - as their obese customers eat less Big Macs and carby candy bars.

To highlight the potential impact of the growing use of GLP-1 drugs, we linked to a Morgan Stanley presentation (available to pro subs) on Thursday that shows a likely 1.7% reduction (vs baseline) in calories consumed.

Not surprisingly, MS found a more pronounced impact on certain food categories among those on the weight-loss drugs.

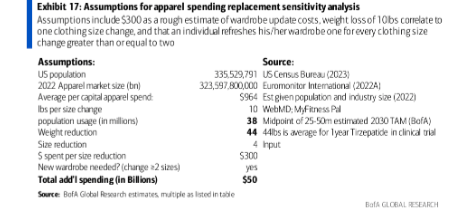

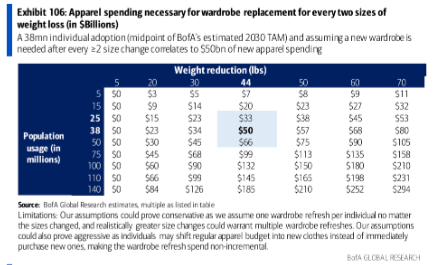

Expanding on MS' report is Bank of America analyst Geoff Meacham (available to pro subs), who reveals the downstream effects of the obesity drug will impact the apparel industry as "eventual weight loss in the broader population could spur a wardrobe replacement cycle."

Meacham said that an adoption rate of 38 million individuals using weight-loss drugs (midpoint of BofA's estimated 2030 TAM) combined with the assumption of buying new clothing could result in $50 billion of new apparel spending.

"The average US womenswear size is 16 - 18 (XL - XXL), according to the US Department of Health and Human Services, which is up from a size 14 a decade earlier. Weight loss could aid demand for the offerings from traditional retailers (who often carry sizes up to 14), and less demand for plus size retailers like Torrid (CURV)," the analyst said, adding, "athletic apparel brands like Lulu Lemon and Deckers (LULU, DECK) to benefit given the healthier lifestyles shown to be supported by GLP - 1 drug."

However, the analyst pointed out a key assumption that depends on whether the heavily indebted consumer can afford new clothes:

"If individuals using GLP - 1 save money through lifestyle changes, they could use this money to fund the clothing spending. As adoption moves towards lower income consumers, this added growth looks less likely and we would expect the customer to trade down to lower priced items to fund spending on new clothes."

In a separate report, John Furner, the chief executive officer of Walmart's sprawling US operation, said they've been comparing shoppers who pick up appetite-suppressing medications at its pharmacies to shoppers who are otherwise similar but aren't filling those scripts at Walmart and noticed those using anti-fat drugs are spending less on food.

"We still expect food, consumables, and health and wellness primarily due to the popularity of some GLP-1 drugs to grow as a percent of total in the back half," Walmart CEO Doug McMillon said on a call with analysts in August.

The BofA analyst adds, "The impact of these downstream effects is much less clear to the market but could change consumer behavior over the longer - term with some industries benefitting while others having higher risk. To this end, we've evaluated the impact that broad adoption of GLP-1 drugs could have on consumer-focused sectors, including 1) snacks and beverages, 2) restaurants, 3) tobacco, 4) gaming, 5) apparel, and 6) food retail."

Updates to Retail Dive’s bankruptcy tracker have been numerous in 2023 so far, with the all-important holiday quarter left to go.

A wide array of U.S. businesses have struggled this year. In the first nine months of 2023, commercial Chapter 11 bankruptcies have soared 61% year over year to 4,553, according to Epiq Bankruptcy, which provides U.S. bankruptcy filing data.

Small business filings in that time rose 41% to 1,419, according to the research, released by Epiq and the American Bankruptcy Institute. In all, considering every type of bankruptcy, filings in the commercial sector rose 17% to 18,680.

High-profile retail filings in the first nine months of the year have included David’s Bridal, Bed Bath & Beyond and Party City, and 11 more retailers may be on the brink.

While the numbers of both commercial and individual filings remain below pre-pandemic levels, the increase so far this year is a sign that challenges, including expanding debt, are building, according to American Bankruptcy Institute Executive Director Amy Quackenboss.

“Struggling individuals and companies have an established lifeline through bankruptcy to help steady themselves amid rising interest rates, inflation and increased borrowing costs,” Quackenboss said in a statement.

Consumer distress is also visible, in rising credit card debt and increasing delinquencies on store credit cards, reported by several retailers in recent months. In the second quarter, U.S. consumers’ collective balance rose to a record $1.03 trillion dollars, according to the New York Federal Reverse Bank’s quarterly report on household debt. That, coupled with the added burden of student loan payments that will resume for many this month, are leading many analysts to temper expectations for holiday sales.

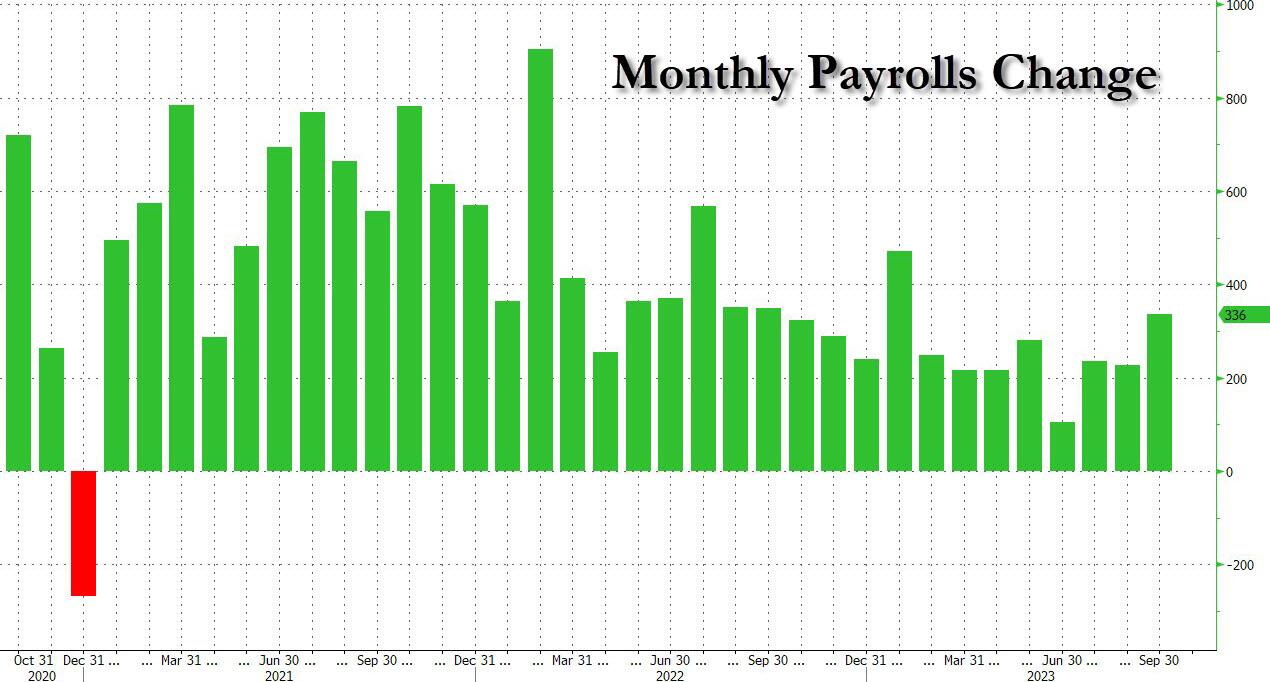

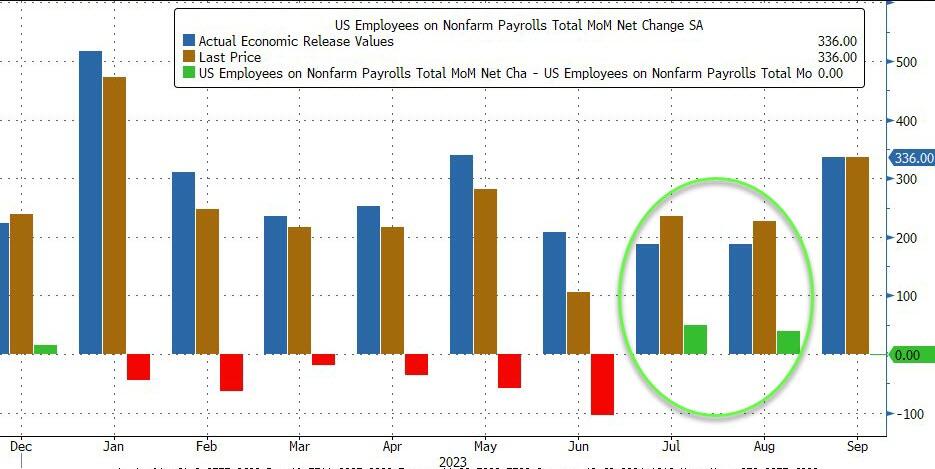

A 6-sigma beat of expectations in non-farm payrolls has sparked chaos across asset classes this morning.

As Academy Securities' Peter Tchir commented: "What a “Weird” Report"

The headline number is shockingly good!

336k jobs created, PLUS 119k of upward revisions! Wow!

But things get a little weird from there:

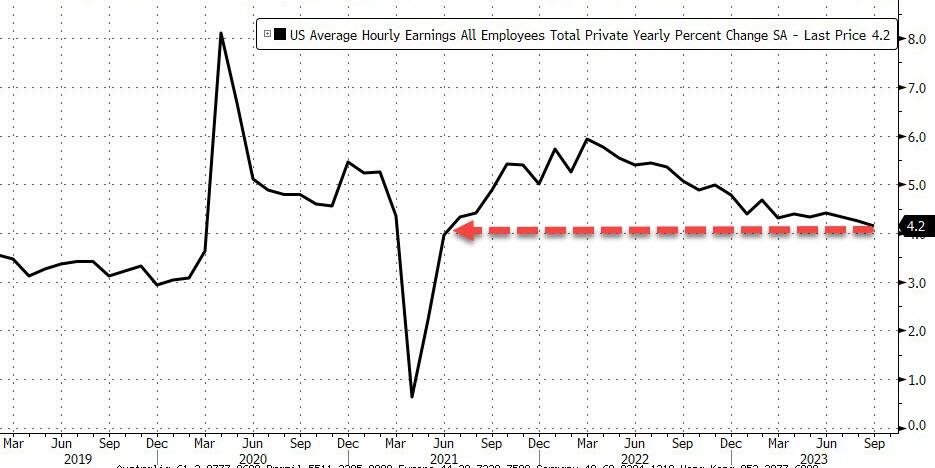

Average hourly earnings stayed at 0.2% (2.4% annualized) and even the annual level came in lower than expectations at 4.2%. Given the strength of the job market (according to the Establishment data) and the barrage of “strike” headlines, that seems somewhat surprising.

Average hours worked remained unchanged at a moderate 34.4 (would expect that to have been stronger last month and this month, given the alleged jobs that were created in the Establishment Survey).

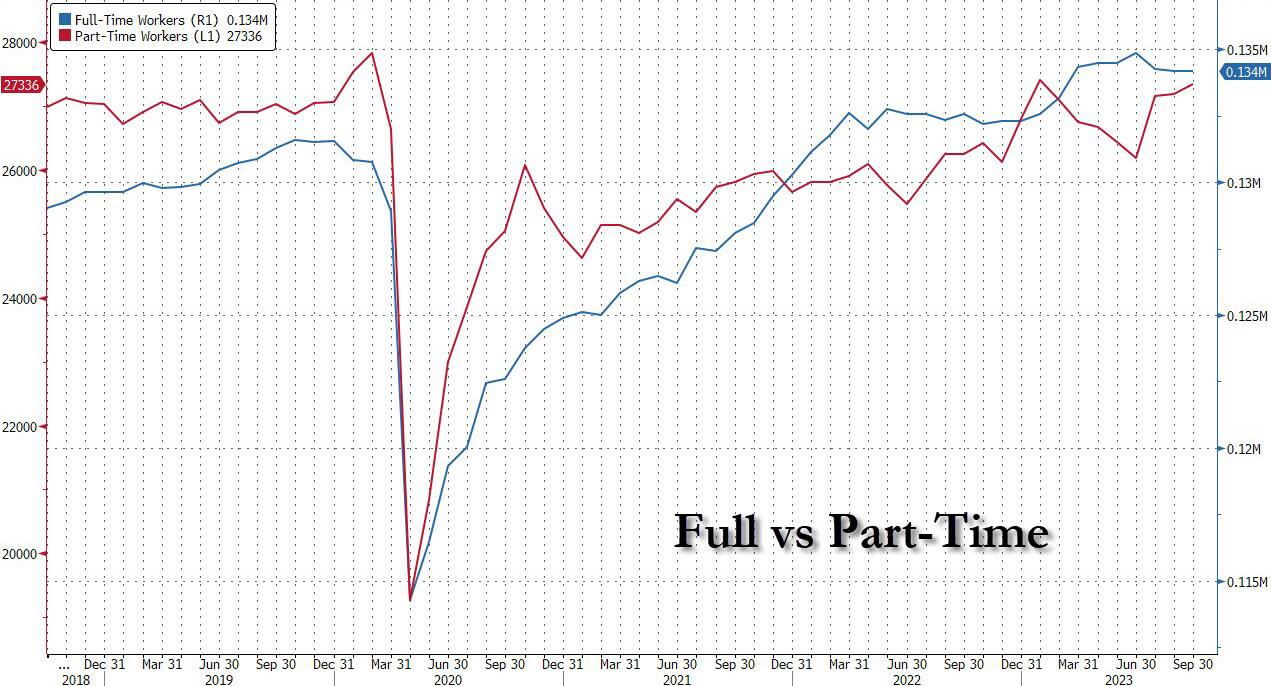

The unemployment rate stayed at 3.8%, as the Household survey showed decline in full-time jobs for the 3rd month in a row. Total jobs were positive for the Household survey, but driven by an increase in part-time jobs (which doesn’t seem overly consistent with a blow out jobs report).

Survey response rates seem to continue to decline (according to the BLS, for the June surveys only 41.7% of potential respondents, responded on the Current Employment Statistics Survey. Which is way better than the 31.9% response rate for JOLTS. When less than 50% of the ticket holders show up for an event, how good is the event? (or in this case, the data?)

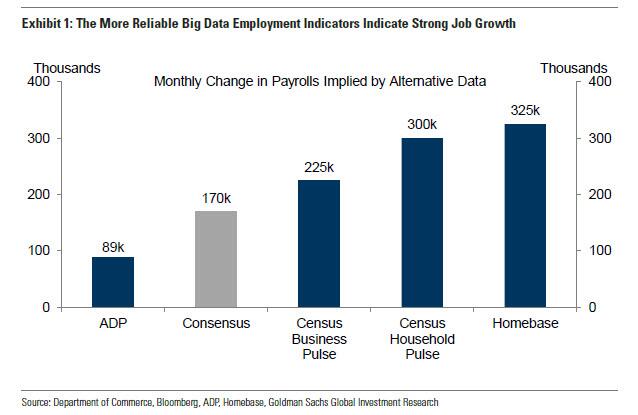

Maybe the hiring is that good, but it didn’t show up ADP, which I suspect, increasingly, ADP has better data than the BLS as it is more dependent on actual, ADP data, than mediocre response rates to surveys.

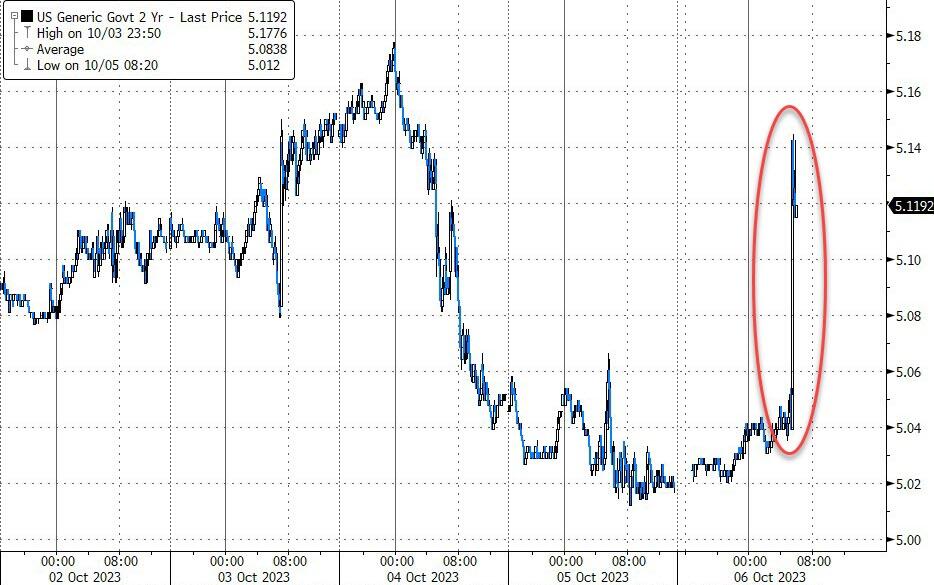

The instant reaction was hawkish and rate-change expectations have shifted notably higher...

And treasury yields are surging - up around 10-15bps across the entire curve...

2Y bounced off close to 5.00%...

Equity futures immediately puked lower, led by Nasdaq...

The dollar is spiking...

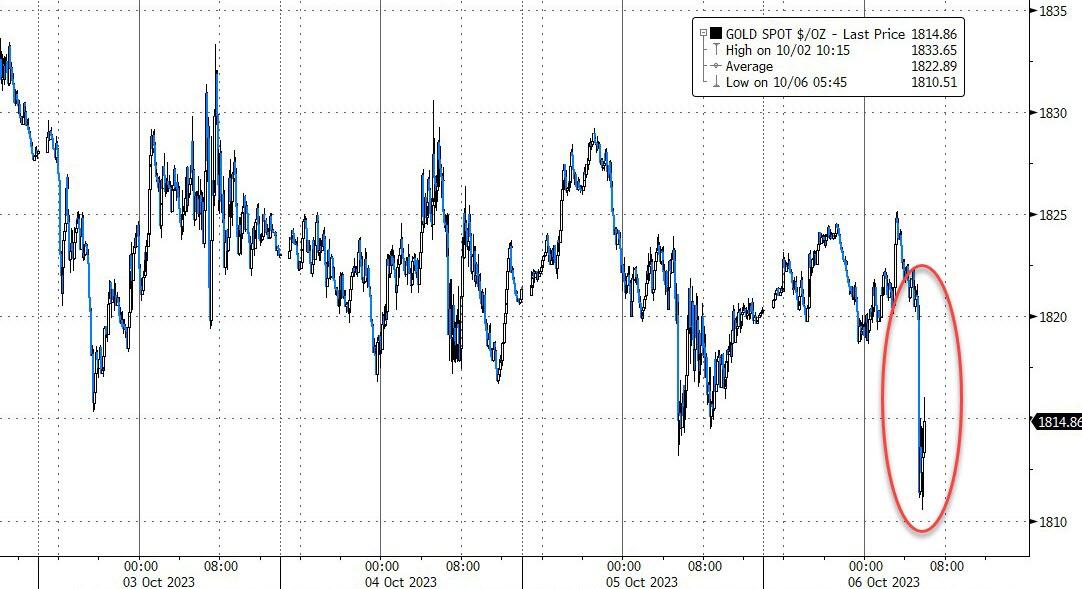

...and gold is dumping again...

Will all this kneejerk action hold? Academy Securities' Peter Tchir is doubtful:

"Difficult to fight the algos which are going to drive yields higher based on the headline number, but expect, as the day goes on, for many in the markets to question the veracity of this report and for the early losses in bonds and stocks to be dramatically reduced, if not finish the day and the week in the green! "

The Biden administration has really outdone itself.

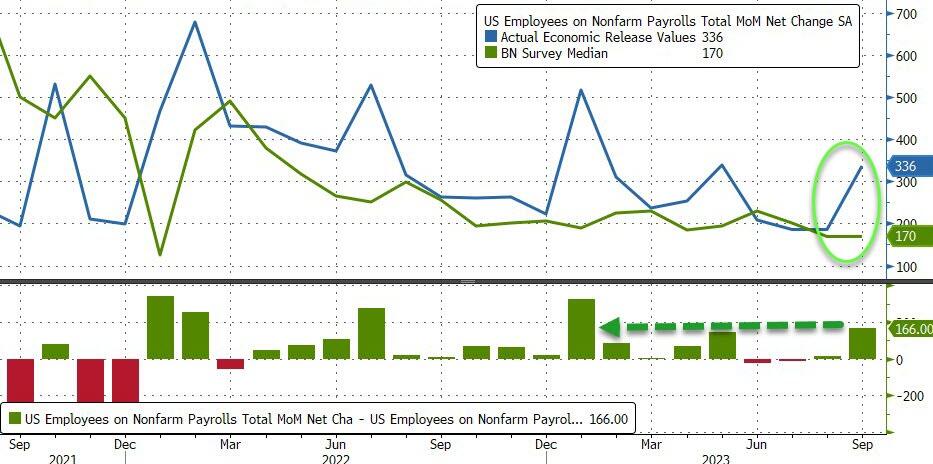

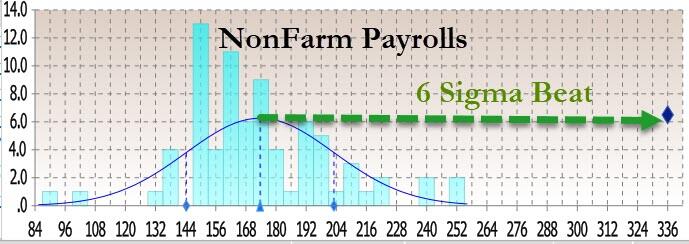

With everyone - even the most hardened bulls - expecting the September jobs report to be not only the weakest of 2023 but to presage a big drop in future payrolls data, moments ago the BLS reported that in September - a month when countless companies shut down due to labor strikes (i.e., people not working) - the US added a whopping 336K jobs, the highest monthly increase since January...

... and not only double the consensus estimate of 170K, but above the highest sellside estimate of 250K!

In fact, at 336K vs a median forecast of 170K, today's print was the first 6-sigma beat of expectations in a long time.

Furthermore, having become the butt of all data goalseeking jokes in recent months after revising every single month in 2023 lower, the BLS decided to show people who is boss and revised not only August but also July higher: the change in total nonfarm payroll employment for July was revised up by 79,000, from +157,000 to +236,000, and the change for August was revised up by 40,000, from +187,000 to +227,000. With these revisions, employment in July and August combined is 119,000 higher than previously reported.

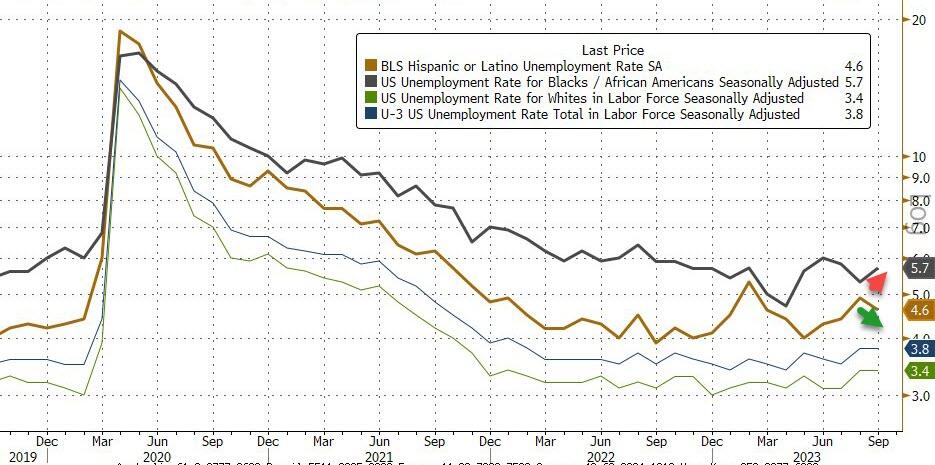

Looking at the unemployment rate, things here were not quite so good, with the rate unchanged at 3.8% from last month, above expectations of a modest drop to 3.7%, as Black unemployment increased while Hispanic unemp dropped.

Unemployment rates were as follows: adult men (3.8%), adult women (3.1%), teenagers (11.6%), Whites (3.4%), Blacks (5.7%), Asians (2.8%), and Hispanics (4.6%).

Meanwhile wage growth continued to cool, and in September average hourly earnings increased 0.2%, below the 0.3% expected, and resulted in a 4.2% increase YoY, down from 4.3% in August...

... as a result of a big bump in lower paying jobs.

But perhaps the most remarkable divergence in the report is that with headline payrolls surging 336K (establishment survey), the Household Survey indicated that the pain continues, as the number of people employed not only rose by less than 100K (86K to be precise), but it was all part-time workers, which increased by 151K. Full-time workers? Why, they dropped by 22K, and the lowest since February.

Some more highlights from the report:

The number of long-term unemployed (those jobless for 27 weeks or more) was little changed at 1.2 million in September. The long-term unemployed accounted for 19.1 percent of all unemployed persons.

Both the labor force participation rate, at 62.8 percent, and the employment-population ratio, at 60.4 percent, were unchanged over the month.

The number of persons employed part time for economic reasons, at 4.1 million, changed little in September. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs.

In September, the number of persons not in the labor force who currently want a job was 5.5 million, little different from the prior month. These individuals were not counted as unemployed because they were not actively looking for work during the 4 weeks preceding the survey or were unavailable to take a job.

Among those not in the labor force who wanted a job, the number of persons marginally attached to the labor force changed little at 1.5 million in September. These individuals wanted and were available for work and had looked for a job sometime in the prior 12 months but had not looked for work in the 4 weeks preceding the survey. The number of discouraged workers, a subset of the marginally attached who believed that no jobs were available for them, also changed little over the month at 367,000.

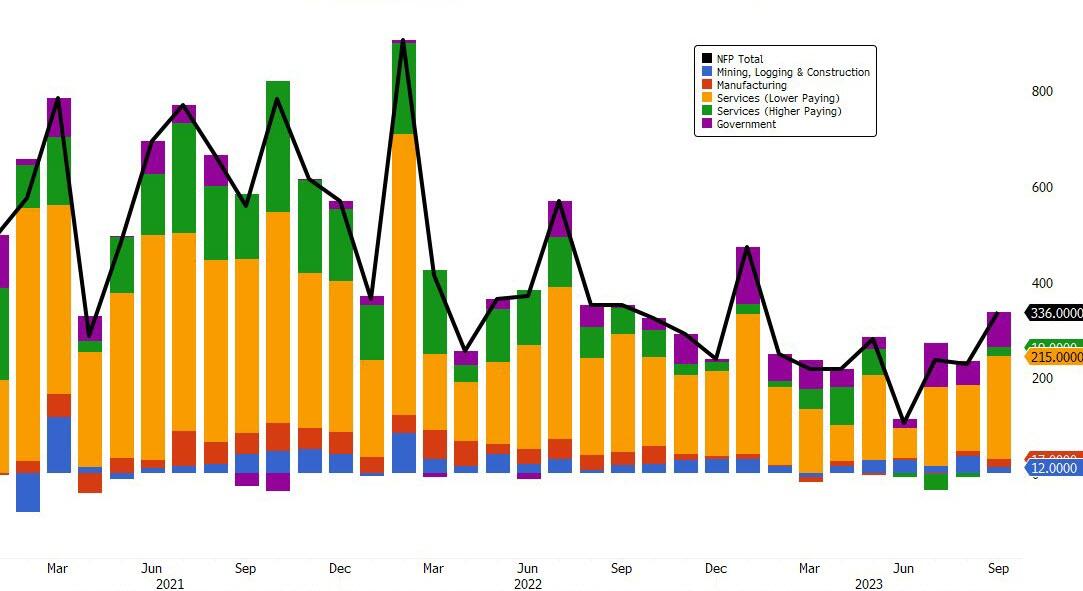

Here is the breakdown of jobs:

Leisure and hospitality added 96,000 jobs in September, above the average monthly gain of 61,000 over the prior 12 months. Employment in food services and drinking places rose by 61,000 over the month and has returned to its pre-pandemic February 2020 level.

In September, government employment increased by 73,000, above the average monthly gain of 47,000 over the prior 12 months. Over the month, job gains occurred in state government education (+29,000) and in local government, excluding education (+27,000).

Health care added 41,000 jobs in September, compared with the average monthly gain of 53,000 over the prior 12 months. Over the month, employment continued to trend up in ambulatory health care services (+24,000), hospitals (+8,000), and nursing and residential care facilities (+8,000).

Employment in professional, scientific, and technical services increased by 29,000 in September, in line with the average monthly gain of 27,000 over the prior 12 months.

Social assistance added 25,000 jobs in September, about the same as the average monthly gain of 23,000 over the prior 12 months. Over the month, job growth occurred in individual and family services (+19,000).

In September, employment in transportation and warehousing changed little (+9,000). Truck transportation added 9,000 jobs, following a decline of 25,000 in August that largely reflected a business closure. Air transportation added 5,000 jobs in September.

Employment in information changed little in September (-5,000). Within the industry, employment in motion picture and sound recording industries continued to trend down (-7,000) and has declined by 45,000 since May, reflecting the impact of labor disputes.

Employment showed little change over the month in other major industries, including mining, quarrying, and oil and gas extraction; construction; manufacturing; wholesale trade; retail trade; financial activities; and other services.

While we will publish a longer reaction piece shortly, this kneejerk response stood out from Peter Tchir of Academy Securities:

Given the strength of the job market (according to the Establishment data) and the barrage of “strike” headlines, that seems somewhat surprising.... The unemployment rate stayed at 3.8%, as the Household survey showed decline in full-time jobs for the 3rd month in a row. Total jobs were positive for the Household survey, but driven by an increase in part-time jobs (which doesn’t seem overly consistent with a blow out jobs report).

Difficult to fight the algos which are going to drive yields higher based on the headline number, but expect, as the day goes on, for many in the markets to question the veracity of this report and for the early losses in bonds and stocks to be dramatically reduced, if not finish the day and the week in the green!

The bottom line seems to be that virtually nobody believes the goalseeked propaganda spewed by the Biden admin any more...

If ever there was a shred of doubt about Elon Musk's intentions to move more volume at lower prices for Tesla this year, those thoughts should officially be put to bed.

Tesla shares are dipping slightly lower on Friday morning after it was reported late Thursday night that Tesla would be making even more price cuts to its Model 3 and Model Y vehicles.

The new cuts to model prices are as follows:

Model 3 Now $38,990 From $40,240

Model 3 Performance Now $50,990 From $53,240

Model 3 Long Range Price Cut To $45,990 From $47,240

Model Y Long Range Now $48,490 From $50,490

Model Y Performance Now $52,490 From $54,490

So far, the price cuts have been a winning formula for Tesla, allowing the automaker to remain at the tip of the demand spear in a global EV race that is now beyond super-saturated with competition.

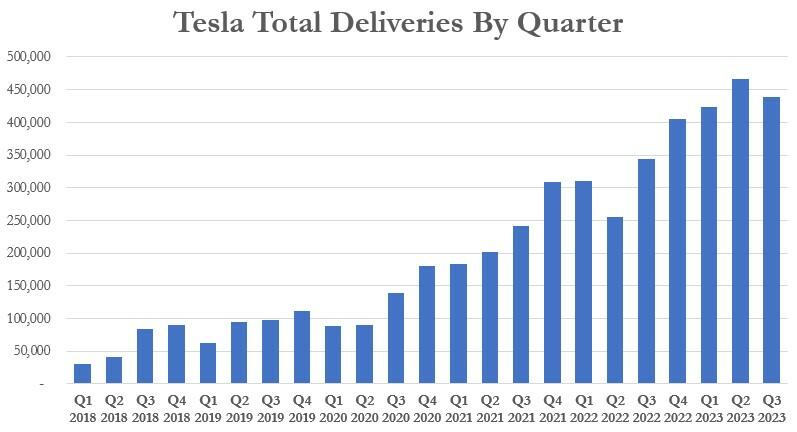

The price cuts come just days after Tesla missed its modest Q3 delivery estimates. In Q3, the company delivered 435,059 vehicles and produced 430,488 vehicles, missing consensus delivery estimates of 456,722.

The quarter marked the first sequential drop in total deliveries since Q2 2022. Prior to that, the last sequential drop in total deliveries occurred in early 2020, as the chart below shows.

The company acknowledged the miss and chalked it up to downtime, stating in its press release the "sequential decline in volumes was caused by planned downtimes for factory upgrades, as discussed on the most recent earnings call."

CEO Elon Musk had said on the company's last conference call that it would “continue to target 1.8 million vehicle deliveries this year.” However, he also warned about production numbers dwindling due to "summer shutdowns for a lot of factory upgrades.”

Analyst Gordon Johnson of GLJ Research called the price cuts a "Midnight Price Cut Massacre" in a note out Friday morning, and suggested that the Q3 miss was not due to line upgrades, but rather due to lack of demand.

"Tesla is already resorting to margin-destroying price cuts just five days into the fourth quarter of 2023," he wrote. "Despite selling only 4,500 more cars than it produced in the third quarter and entering the fourth with a record inventory of 106,000 cars, it's clear that Tesla's issues rest mainly with lackluster demand."

"This means to hit its goal of 1.8mn cars produced in 2023, Tesla may have to sell those cars at negative net income margins," he continued.

Analyst Mark Delaney wrote in a note in September: “We believe that Tesla could further lower prices in 2024 to support higher volumes, which we believe will mitigate the EPS benefit from cost reductions.”

The note continued: “We lower our 2023 and 2024 EPS estimates for Tesla, mostly on lower ASPs and, in turn, auto gross margin ex-credit assumptions (driven by lower prices for S/X and, to a lesser extent, Model Y, and partly offset by higher Model 3 ASP assumptions)."

Goldman called the company's price cuts into question, noting they could have a negative effect on Tesla's bottom line, Teslarati reported:

“Tesla materially reduced S/X pricing on 9/1 by 15-19%, and reduced Model Y pricing in China in mid-August (and has been discounting inventory on hand in other markets like the US this quarter). However, Tesla raised pricing on the Model 3 with the refreshed version (Highland) that is now being sold in Europe and China.”

But it wasn't all criticism over price cuts. Canadian VC and self-labeled "SPAC Jesus" Chamath Palihapitiya was out over Labor Day weekend praising the speed and aggressiveness of Tesla's price cuts, which ultimately do seem to be moving metal.

"Some companies cut prices, but most keep prices flat or increase them," he added. "Some companies improve products quickly. But no one has actually given you more for less on such a big ticket purchase so frequently."

Recall, we also noted in August that Tesla had cut the price of its Model S Plaid in China by 19%.

By Garfield Reynolds, Bloomberg markets live reporter and strategist

Investors are anticipating the Federal Reserve is close to the end of its tightening cycle.

Every surge in bond yields spurs fresh speculation the economy will break badly enough for policy makers to pivot rapidly away from their hawkish stance. That may set up bonds and stocks for a tough time even if Friday’s payrolls report comes in on the soft side.

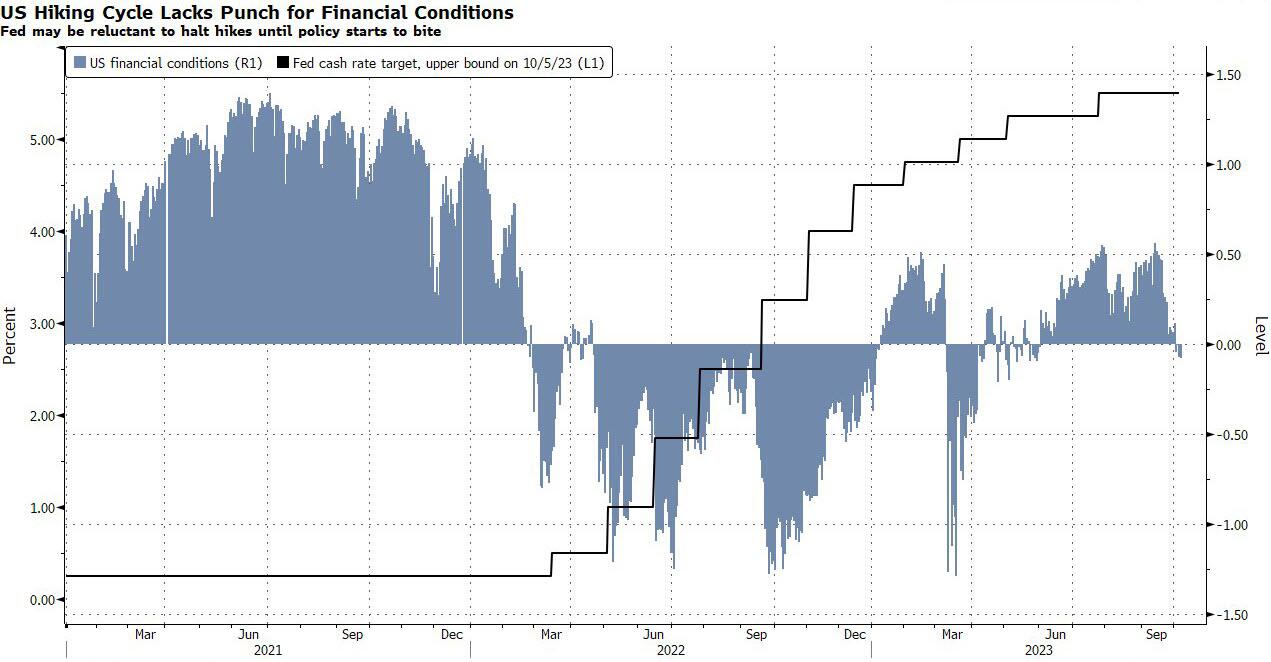

That’s because even the recent rout in Treasuries only managed to push US financial conditions to a neutral level, based on a Bloomberg gauge, well short of the sort of restrictive impact the Fed would seem to be wanting to achieve. That also helps explain the still-resilient state of the economy � Bloomberg’s US data surprise index remains at elevated levels.

A softer set of labor data is still unlikely to be stunningly bad enough to quiet the Fed hawks. But it could well set off a strong relief rally in most assets as investors move further toward pricing in an end to rate hikes that policymakers would have little sympathy for.

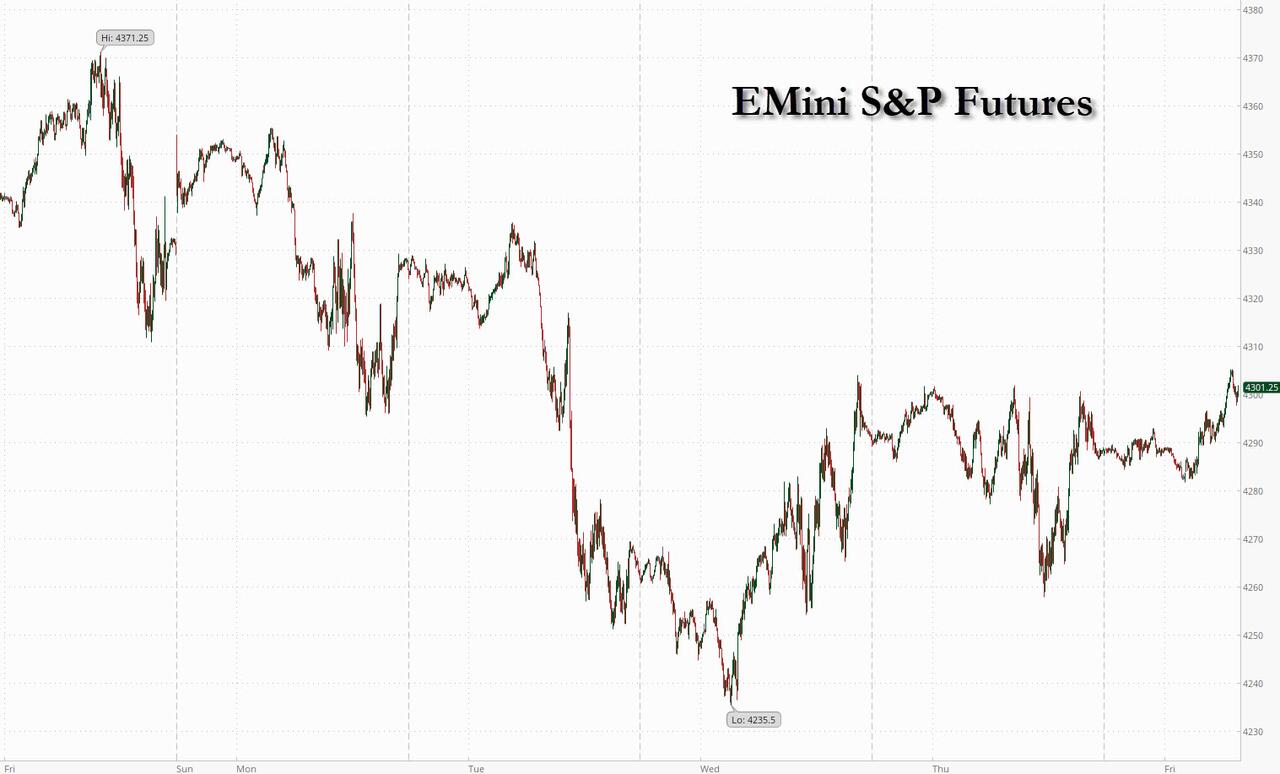

Global stocks and US index futures gained ahead of the September payrolls report (exp. payrolls 170K, unemp 3.7%, full preview here) that could potentially ease pressure on the Federal Reserve to raise interest rates again. At 7:45am ET, S&P futures rose 0.1%, after falling by a similar amount on Thursday while the tech-heavy Nasdaq 100 rose 0.2%, after slipping 0.4% the day before. Shares climbed in Asia and Europe, while mainland Chinese markets remain shut for a weeklong holiday. Treasury yields extended their advance, with the 10-year hovering around 4.74% after reaching 4.88% earlier this week. The Bloomberg dollar index was little changed. Oil was also little changed, halting its decline this week. All eyes on today’s NFP release at 8.30am, which is the near-term focus to set narrative: consensus expects NFP to print 170k and the unemployment rate to print 3.7%.

In premarket trading, shale giant Pioneer Natural rose as much as 10% after WSJ reported that Exxon Mobil is in talks to acquire the company. Exxon Mobil fell as much as 2.1%. Tesla fell as much as 1.6% as the electric-vehicle maker cut prices on its most popular cars in the US. Here are some other notable premarket movers:

Aehr Test Systems fell as much as 14% after the supplier of semiconductor test and production burn-in equipment reported its first-quarter results.

AMC Entertainment Holdings Inc. gained 2.8% after it said it sold more than $100 million in advance tickets for the Taylor Swift/The Eras Tour Concert movie.

Elf Beauty rose as much as 2.5% as Jefferies raised to buy from hold. The broker says it sees a buying opportunity following the recent valuation pullback in the cosmetics company. .

Shoals Technologies Group rose as much as 4% as Piper Sandler raised to overweight from neutral. The broker said it’s upgrading the solar-energy equipment maker after the recent pullback in its shares. .

Today's nonfarm payrolls report is forecast to show employers slowed hiring last month, with 170,000 jobs being added last month, down from 187,000 in August. The crowdsourced whisper number is 190k, while Goldman warns that big data indicators hint at an even larger beat. In any event, this is expected to be the last to show solid hiring before a sharp slowdown.

Job data earlier this week provided a discordant narrative: job-openings overshot estimates, while a measure of private employment from ADP was weaker than forecast. Here is a forecast of payrolls by bank (with our full preview available here).

240,000 - Citigroup

200,000 - Goldman Sachs

200,000 - UBS

190,000 - HSBC

190,000 - Societe Generale

180,000 - Morgan Stanley

175,000 - JP Morgan Chase

173,000 - Bloomberg Economics

150,000 - Deutsche Bank

150,000 - Wells Fargo

“Although both numbers haven’t been moving in tandem recently, the lower-than-expected ADP figures have given markets hope that September nonfarm payrolls will surprise to the downside,” said Julien Lafargue, chief market strategist at Barclays Private Bank. “Beyond the number of job creations, investors will pay close attention to wage growth figures and whether they confirm recent disinflationary trends.”

Meanwhile, the global bond selloff is hammering risk assets from stocks to corporate credit on concerns that central banks will keep interest rates elevated longer than expected. While 30Y yields this week touched 5% for the first time since 2007 and subsequently dropped, on Friday Treasury yields once again extended their advance, with the 10-year adding two basis points to 4.74% after reaching 4.88% earlier this week. A gauge of dollar strength was little changed.

The beaten-down bond sector will make a staggering comeback in 2024 when higher interest rates send the economy into a recession, according to BofA's Michael Hartnett. Once the recession being priced by bond and stock markets “mutates into economic data, bonds rally big and bonds should be the best performing asset class in the first half of 2024,” Hartnett wrote in a note.

“Friday’s payrolls data, and next week’s inflation number, will decide whether the 10-year Treasury yield goes up to 5% or down to 4.5%,” said Kenneth Broux, a strategist at Societe Generale in London. A higher-than-forecast jobs number may trigger “another wave of dollar-buying and bond-selling,” he said.

Traders have record sums riding on the outcome of November’s Fed meeting as investors and policymakers debate the likelihood of a further rate increase this year. San Francisco Fed President Mary Daly, who doesn’t vote on the Fed’s rate-setting committee this year, said the central bank may keep rates on hold if inflation and the jobs market cool.

In Europe, the Stoxx 600 rose as much as 0.8%, extending earlier advance as bond yields remain in Thursday’s range and gains in dollar pause ahead of US job data. FTSE MIB outperforms peers. Insurance +2% and banks +1.6% lead gains; Food and beverages -1.5% and personal care -0.9% are the only sectors in the red. Insurers led gains in Europe’s Stoxx 600 index, after Aviva Plc was cited in a newspaper as a target for potential bidders. Prudential, Legal & General Group and Phoenix also rose. Here are the most notable European movers:

Shell shares rise as much as 1.5% after it says its earnings from gas trading rebounded in the third quarter from the dip seen in the prior period.

Aviva shares rise as much as 8.3% to 420.40p after The Times reported market speculation that the insurer may be attracting interest from at least two potential bidders.

Man Group gains as much as 4.6%, most since Mar. 21, after BNP Paribas Exane raised its recommendation on the UK-listed hedge fund to outperform from neutral.

Maire shares gain as much as 7.5% as Mediobanca upgrades the technology and engineering group to outperform from neutral, after it won the largest order in the group’s history.

Nestle shares drop as much as 3.4% to the lowest since March 2021, biggest laggard in Europe’s Stoxx 600 Index by index points. Retail giant Walmart said Wednesday that it’s already seeing an impact on shopping demand from people taking Ozempic, Wegovy and other appetite-suppressing medications.

Philips shares fall as much as 8.5%, the most in a year, after the company said it agreed with the US FDA recommendations to implement additional testing on certain sleep and respiratory care devices to supplement current test data.

JD Wetherspoon falls as much as 4.8%, the most in two months, as Morgan Stanley notes the UK pub chain now anticipates a “reasonable outcome” for the 2024 fiscal year, versus the “improved outcome” guidance provided at 4Q results. Wetherspoon said it returned to profit in the 12 months through July.

CD Projekt shares widen two-day decline to 12% as analysts point to negative surprise concerning the cost of production of the Phantom Liberty paid add-on to its Cyberpunk 2077 game that may limit profits from the new release.

Earlier in the session, Asia stocks also gained, led by a rally in Hong Kong shares, while other markets were more muted with all eyes on the US payroll data for cues on the Federal Reserve’s policy path. The MSCI Asia Pacific Index rose as much as 0.7% Friday, paring its slide for the week to 1.4%. It would be the third consecutive week of declines for Asian stocks. Chinese tech giants Tencent, Alibaba and Meituan were among the biggest contributors to the gauge’s advance. The benchmark tumbled into a technical correction earlier this week amid concern over higher-for-longer US rates. Hong Kong stocks were the biggest gainers in the region, with analysts citing positive Golden Week holiday spending data and positioning ahead of the reopening of mainland markets as drivers. Japan equities were mixed while benchmarks in Australia and South Korea edged higher.

Hang Seng outperformed amid strength in tech, property and banking stocks, with sentiment also underpinned by hopes of a stabilisation in US-China ties as the White House is reportedly planning a Biden-Xi meeting in California next month although nothing has been confirmed yet.

Japan's Nikkei 225 was choppy as better-than-expected Household Spending data was offset by slower wage growth, while former BoJ official Momma said the BoJ will likely discuss whether to tweak forward guidance along with YCC at the end-October meeting.

Australia's ASX 200 was led by gains in the top-weighted financial sector after the latest RBA Financial Stability Review which noted increasing global financial stability risks but also stated that Australian banks are well-capitalised and well-positioned to manage any increase in mortgage arrears and absorb loan losses.

Indian stocks gain for a second day, supported by a pause on interest rates by the central bank and gains in the technology and capital goods companies. The S&P BSE Sensex rose 0.6% to 65,995.63 in Mumbai on Friday, while the NSE Nifty 50 Index advanced by the same measure. The MSCI Asia Pacific Index was up 0.5%.

In FX, the Bloomberg dollar spot index erased an earlier advance. GBP and CAD are the strongest performers in G-10 FX, JPY and AUD underperform.

The EUR/USD pared a 0.2% drop to trade little changed at 1.0552. The pair is down a 12th week, the longest streak of losses since 1997.

GBP/USD rose 0.1% to 1.2203, heading for a third daily advance for the first time since August

The yen led declines among Group-of-10 currency peers. USD/JPY extended gains, rising as much as 0.3% to 148.99 after Japan’s slower-than-expected wage growth suggests the Bank of Japan has to wait more to normalize policy

In rates, treasuries were slightly cheaper across the curve ahead of September jobs report, with futures trading just off Thursday session highs, as stock futures hold small gains. Gilts underperformed in early London session, adding to upside pressure on Treasury yields, while WTI oil futures are little changed after past week’s collapse. US yields 2bp-3bp cheaper with curve spreads little changed on the day; 10-year TSYs were around 4.74%, around the middle of Thursday’s range, with gilts lagging by 1.5bp in the sector. Gilt 10-years slightly underperform comparable bunds and USTs. A survey by BMO Capital Markets on client attitudes toward rates market found the lowest willingness to buy in a year � 37% vs a 49% average � if bond prices fall after the jobs report. The Dollar IG issuance slate empty so far and expected to be muted Friday ahead of Monday’s bank-and-bond-market holiday; three names priced $2.5b Thursday, taking weekly volume to almost $9b, below the $15b projected

In commodities, oil trades slightly higher on the day, but is poised for the biggest weekly drop since March. Spot gold is little changed at $1,820/oz.

Looking at the day ahead, today's US economic data slate includes September jobs report (8:30am) and August consumer credit (3pm). Scheduled Fed speakers include Waller at 12pm

Market Snapshot

S&P 500 futures little changed at 4,290.50

MXAP up 0.4% to 154.81

MXAPJ up 0.8% to 486.12

Nikkei down 0.3% to 30,994.67

Topix little changed at 2,264.08

Hang Seng Index up 1.6% to 17,485.98

Shanghai Composite up 0.1% to 3,110.48

Sensex up 0.6% to 66,024.33

Australia S&P/ASX 200 up 0.4% to 6,954.17

Kospi up 0.2% to 2,408.73

STOXX Europe 600 up 0.4% to 442.89

German 10Y yield little changed at 2.90%

Euro little changed at $1.0543

Brent Futures up 0.4% to $84.41/bbl

Gold spot down 0.0% to $1,819.92

U.S. Dollar Index little changed at 106.42

Top Overnight News

The White House has begun making plans for a November meeting in San Francisco between President Biden and Chinese leader Xi Jinping � an attempt to stabilize the relationship between the world’s two most powerful countries, according to senior administration officials. WaPo

India’s RBI keeps rates unchanged, as expected, but suggested it would hold policy tight going forward due to ongoing inflation concerns. WSJ

Beijing’s tough treatment of foreign companies this year, and its use of exit bans targeting bankers and executives, has intensified concerns about business travel to mainland China. Some companies are canceling or postponing trips. Others are maintaining travel plans but adding new safeguards, including telling staff they can enter the country in groups but not alone. WSJ

Russia allowed a return to seaborne exports of diesel just weeks after imposing a ban that roiled global markets, taking other steps instead to keep sufficient fuel supplies at home. BBG

European gas jumped as union members at Chevron LNG facilities in Australia voted to resume industrial action after criticizing the company's efforts to finalize a deal on pay and conditions. BBG

The ECB may need to raise interest rates again if wages, profits or new supply snags boost inflation, ECB board member Isabel Schnabel said in an interview published on Friday. RTRS

Tesla cut prices on its Model 3 and Y cars in the US again, days after its third-quarter deliveries missed. BBG

The corporate borrowing binge over the past 18 months shows C-suites across the US have been largely undeterred by the Fed's relentless hikes. Not only have they displayed little desire to pay down debt, but many have heaped more of it on their books. The recent yield spike may have cooled the market, but the overall pace of borrowing has been blistering. BBG

Exxon is in talks to acquire Pioneer Natural Resources, a person familiar said. An agreement worth as much as $60 billion may completed within days, the WSJ reported, making it the world's largest deal this year and Exxon's biggest acquisition in over two decades. WSJ

We estimate nonfarm payrolls rose by 200k in September (mom sa), above consensus of +170k. We estimate that the unemployment rate declined one tenth to 3.7%� in line with consensus� reflecting a rise in household employment and unchanged labor force participation at 62.8% (we do not expect the August rise in the foreign-born labor force to reverse). We estimate a 0.30% increase in average hourly earnings (mom sa) that edges the year-on-year rate lower by 1bp to 4.28%, reflecting waning wage pressures but positive calendar effects (the latter worth +5bps month-over-month, on our estimates). Consensus for average hourly earnings is +0.3% mom and +4.3% yoy. GIR

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly higher albeit with some of the upside capped following the inconclusive performance on Wall St and as participants await the incoming US Non-Farm Payrolls report. ASX 200 was led by gains in the top-weighted financial sector after the latest RBA Financial Stability Review which noted increasing global financial stability risks but also stated that Australian banks are well-capitalised and well-positioned to manage any increase in mortgage arrears and absorb loan losses. Nikkei 225 was choppy as better-than-expected Household Spending data was offset by slower wage growth, while former BoJ official Momma said the BoJ will likely discuss whether to tweak forward guidance along with YCC at the end-October meeting. Hang Seng outperformed amid strength in tech, property and banking stocks, with sentiment also underpinned by hopes of a stabilisation in US-China ties as the White House is reportedly planning a Biden-Xi meeting in California next month although nothing has been confirmed yet.

Top Asian News

TSMC (2330 TT/TSM) September sales: (TWD) 180.43bln (prev. 188.69bln in Aug; -13% Y/Y), according to Reuters.

A 6.1 magnitude earthquake has struck southeast of Honshu, Japan, according to GFZ.

European bourses trade on the front foot as indices attempt to recoup lost ground with the Stoxx 600 on track to close the week out with losses of over 1.5%. Sectors in Europe are mostly firmer with the current outperformers being Insurance, Banks, and Tech, while Food Beverages and Tobacco, Optimised Personal Care Drugs and Grocery, and Utilities reside as the laggards. US futures are trading marginally firmer, with overall sentiment tentative ahead of the big NFP report, expected to be released at 13:30 BST / 08:30 ET.

Top European News

German Government expects GDP to decline by 0.4% in 2023 in draft Autumn projections, according to Reuters citing sources. German government foresees GDP growth of 1.3% in 2024 and 1.5% in 2025 and expects inflation of 6.1% in 2023 and 2.6% in 2024. Reasons for the expected mild GDP contraction in 2023 are high energy prices, high inflation and weakness in international trade, via Reuters citing German Government Source

FX

DXY is caged to a tight 106.34-55 with FX markets generally steady in the run-up to the US jobs report.

Pound perked up enough in early trade to probe 1.2200 and decent expiry interest at the round number.

EUR/USD secured a firmer grasp of the 1.0500 handle having closed bullishly above the 10 DMA yesterday.

Kiwi and Aussie are underpinned by a pick-up in broad risk appetite rather than specifics.

Fixed Income

Bond futures have plateaued and pushed the bounds of recovery far enough ahead of the US jobs data - which has the potential to move the dial or even alter the overall trend.

Bunds are close to 128.00 within their 128.17-127.79 intraday range having peaked on Monday at 128.50 and troughed at 126.62 on Wednesday.

Gilts are midway between 92.86-53 stalls flanked by 93.71-91.50 w-t-d extremes.

T-note is sitting tight inside 107-10/02 confines compared to a high of 107-29+ and 106-03+ low.

Orders for Italy's new 5-yr BTP Valore retail bond touched EUR 16bln since the beginning of the offer, according to Reuters.

Commodities

Crude futures are choppy with two-way price action seen this morning as the complex consolidates after essentially wiping out its September gains at the start of this month.

Dutch TTF futures are firmer intraday as the Offshore Alliance members at Chevron voted to recommence protected industrial action.

Spot gold is flat within recent ranges while base metals rebounded off worst levels at the start of European trading but gains are capped ahead of the tier 1 US data in the afternoon.

Offshore Alliance members at Chevron (CVX) vote to recommence protected industrial action, according to the union.

Russia lifts diesel export ban via pipelines, according to Ifax.

Central banks

ECB's Schnabel said if risks materialise then further rate hikes may be necessary at some point, according to Reuters.

ECB's Herodotou said monetary policy transmission is taking place to tame inflation, but energy prices and bank liquidity needs monitoring, according to Reuters.

Former BoJ official Momma commented that the BoJ will likely discuss whether to tweak forward guidance along with YCC at the October 30th-31st meeting,

RBA Financial Stability Review stated global financial stability risks are elevated and growing, while the risks include China's property sector, a disorderly fall in global asset prices and exposure to commercial real estate. The FSR also noted that tightening global financial conditions could slow growth and lift unemployment, while a fall in global asset prices could raise funding costs in Australia and limit the supply of credit. Nonetheless, it stated the Australian financial system is sound but there are some pockets of stress among household borrowers and Australian banks are well-capitalised with low exposure to commercial property, as well as well-positioned to manage any increase in mortgage arrears and absorb loan losses.

RBI kept the Repurchase Rate unchanged at 6.50%, as expected, while it maintained the stance of remaining focused on the withdrawal of accommodation in which 5 out of 6 members voted in favour of the policy stance. RBI Governor Das said they have identified inflation as a major risk to macroeconomic stability and remain focused on aligning inflation to the 4% target with the MPC highly alert and will take timely measures as necessary. However, Das commented that headline inflation is to see further easing in September and the silver lining is the declining core inflation, as well as noted that the transmission of past rate hikes is thus far incomplete.

RBI Governor Das said OMO sales are not for yield curve management but for liquidity management. Das added the RBI does not have a specific level in mind for the exchange rate; intervention is to prevent volatility in the FX market, according to Reuters.

CNB Minutes: A large part of the debate was devoted to starting the process of lowering monetary policy rates and pace; the weakening of the FX rate over the past month had delivered a monetary policy easing of roughly 25-50bps, according to Reuters.

US Event Calendar

08:30: Sept. Change in Nonfarm Payrolls, est. 170,000, prior 187,000

Change in Private Payrolls, est. 160,000, prior 179,000

Change in Manufact. Payrolls, est. 5,000, prior 16,000

Unemployment Rate, est. 3.7%, prior 3.8%

Underemployment Rate, prior 7.1%

Labor Force Participation Rate, est. 62.8%, prior 62.8%

Average Weekly Hours All Emplo, est. 34.4, prior 34.4

Average Hourly Earnings YoY, est. 4.3%, prior 4.3%

Average Hourly Earnings MoM, est. 0.3%, prior 0.2%

15:00: Aug. Consumer Credit, est. $11.7b, prior $10.4b

DB's Jim Reid concludes the overnight wrap

Risk assets were under pressure again over the last 24 hours, with investors remaining cautious before today’s US jobs report. For instance, oil prices remained on track for their worst weekly performance since the banking turmoil in March, having now shed more than -11% this week. Credit spreads widened as well, with US HY spreads at their widest in more than 3 months. And whilst it’s true that sovereign bonds did recover some ground for the most part, we did see some new milestones for yields, and the US 30yr real yield (+6.8bps) closed at a post-2008 high of 2.50%. Furthermore, the spread between Italian and German 10yr yields closed above 200bps for the first time since early February. US equities also lost further ground, with the S&P 500 down -0.13% in spite of a late recovery, and there’s been little respite this morning with futures for the index down -0.05%.

With that backdrop in mind, the main highlight today is likely to be the US jobs report for September, which is the last before the Fed’s next decision on November 1. And since pricing for another rate hike this year has kept oscillating above and below 50% (currently 38% this morning), today’s reading will be important in determining if another hike remains on the table. The reading also follows a progressive slowing in job growth over recent months, and in the last report we saw the 3m average for payrolls growth fall to a post-pandemic low of +150k. Then on Wednesday this week, the ADP’s report of private payrolls showed the weakest monthly gain (+89k) since January 2021, which prompted investors to dial back the chances of another rate hike. But on the other hand, the weekly jobless claims yesterday were at 207k (vs. 210k expected) over the week ending September 30, which pushed the 4-week average down to its lowest since early February, at 208.75k. So there are signals pointing in both directions. For today, our US economists are expecting nonfarm payrolls to grow by +165k, which would see the unemployment rate tick down a tenth to 3.7%.

With all that to look forward to, sentiment remained pretty negative in markets and there was a clear risk-off tone for much of the day yesterday. That was very clear in commodity markets, where oil prices continued to slump and Brent Crude fell another -2.03% to $84.07/bbl. Bear in mind that it was at $95/bbl at the start of the week, so with a -11.75% decline over four days, Brent is on track to almost match its worst week of the year back in March (-11.85%). If it’s sustained, this downward pressure could actually be very supportive for central banks as they seek to get inflation back to target. However, the reason it’s slumped is very much based on fears that growth is weakening, which in turn would reduce oil demand. It was a similar story for other cyclical commodities, and copper prices (often taken to be an industrial bellwether) were down -1.03% to a 4-month low. Meanwhile, the rise in real rates meant that gold (-0.06%) remained under pressure, with a 9th consecutive daily fall for the first time since 2016.

When it came to equities, the risk-off mood dominated in the first half of the US session, with the S&P 500 down -0.89% at the lows of the day. But it recovered to end the day with a modest decline of -0.13%. Other US indices, including the NASDAQ (-0.12%), the FANG+ index (-0.14%) and the Russell 2000 (+0.14%), posted similar moves. Over in Europe, the STOXX 600 (+0.28%) ticked up from its 6-month low the previous day, but there still wasn’t much strength across the major indices, and the DAX (-0.20%) closed at a 6-month low.

For sovereign bonds however, the risk-off tone meant they put in a much better performance, not least because investors moved to lower the chances of further monetary tightening. In the US, that meant yields on 10yr Treasuries were down -1.4bps to 4.72%, whilst in Europe there were also declines for yields on 10yr bunds (-4.0bps), OATs (-2.4bps) and gilts (-3.8bps). However, it wasn’t all good news, and longer-dated US Treasuries continued to struggle, with new records set among some real yields. For instance, the 20yr real yield (+6.4bps) hit a post-2009 high of 2.58%, and the 30yr real yield (+6.7bps) hit a post-2008 high of 2.49%. Italian BTPs also lost further ground, and the spread between 10yr BTP yields over bunds closed above 200bps for the first time since early February.

That rates moves came amidst slightly less hawkish comments from Fed and ECB speakers. San Francisco Fed President Daly noted that the rise in yields in September “is equivalent to about a rate hike” and that the Fed can hold rates steady if the cooling of the labour market and inflation continues. Meanwhile, Richmond Fed President Barkin said that “we have time to see if we’ve done enough or whether there’s more work to do”. Over in Europe, Banque de France Governor Villeroy said that as of today he saw “no justification for an additional increase in the ECB rates”. Speaking of central banks, my colleague Peter Sidorov has published a report overnight on global central bank QT. We’ve seen DM central banks’ rundown of bond holdings accelerate in recent months and he observes that this QT pace is yet to peak. See the report here for more on QT trends and their implications.

Overnight in Asia, there’ve been more positive signs in markets, with gains across the major equity indices. The Hang Seng (+1.81%) is leading the way, but there’s also been advances for the KOSPI (+0.26%) and the Nikkei (+0.08%), whilst markets in mainland China remain closed for a holiday. The 10yr Treasury has also seen modest gains overnight, with yields down -0.6bps to 4.71%.

To the day ahead now, and the main highlight will be the US jobs report for September. Other data includes German factory orders and Italian retail sales for August, along with the Canadian employment report for September. From central banks, we’ll hear from the Fed’s Waller, and the ECB’s Knot, Vasle, Vujcic and Kazimir.

Friends of murdered New York City liberal activist Ryan Thoresen Carson have created a GoFundMe page in which the "collective" solicits donations so they can take "time off of work" -- and have already raked in $69,000. However, some donors are chipping in just for the privilege of leaving scathing comments.

Carson was stabbed to death at 3:50 am on Monday in New York's Bedfort-Stuyvesant neighborhood, as he and his girlfriend were returning from a Long Island wedding. They encountered an enraged young man who was kicking over parked mopeds and scooters before turning his rage on Carson, asking, "What the f*** are you looking at? I'll kill you!"

In video that captured the crime, Carson be heard repeatedly telling his assailant to "chill." Carson was stabbed multiple times, including a fatal strike to his heart. (Note: Issuing orders to an enraged man is seldom a sound de-escalation strategy.)

GRAPHIC WARNING: NY Post obtains and releases video showing fatal stabbing of Leftist activist Ryan Carson in front of girlfriend on NYC street late-night after wedding

1. Always carry a gun

2. Always keep distance between yourself and a potential threat

On Thursday, NY cops arrested 18-year-old Brian Dowling -- who lives near the crime scene on Lafayette Avenue near Malcom X Boulevard -- and charged him with murder and criminal possession of a weapon. A search of Dowling's apartment produced a sweatshirt matching the one that appears in security-camera video of the murder, along with a knife. He'd previously received summonses for disorderly conduct, and allegedly smashed items in his girlfriend's apartment. In a 911 call, his aunt described him as mentally disturbed.

Meanwhile, a self-identified "collective of Ryan's close friends" is managing a GoFundMe account on behalf of themselves and Carson's girlfriend Claudia Morales. However, rather than seeking funds for funeral and other final expenses, the group says they need the money "to eas[e] the burden and stress of this horrifying situation so that we can have space and time to grieve." More pointedly, they say "immediate needs are to offset the costs of working class people taking time off of work to properly mourn."

"We hope you may find his thoughts on mutual aid, his works of advocacy, and understand that his radical principles of community care, justice, and dismantling an individualized profit-centered way of life are worth carrying forward," the page says.

As of Thursday night, the GoFundMe page reflected more than 1,300 donations totaling $69,579. However, some small donations have been made by people paying for the opportunity to condemn the group for using Ryan's death to create a time-off fund.

A donor identifying as Scott Adams -- we don't know if it's the Scott Adams -- chipped in $5 and posted "All Cops Are Bastards," echoing the slogan that, in acronym form, adorned a shirt once worn by Carson's girlfriend. She has also been a "Black Lives Matter" activist. Carson, who worked for the New York Public Interest Research Group, campaigned for bottle-deposit laws and supervised drug injection sites.

"It's abhorrent for someone to use the MURDER (not "loss" or "tragedy") of her boyfriend, and his life's work and reputation, to manipulate people to give her loads of cash. His body was barely even cold."

"I donated $5 because it was the minimum but I wanted to say this: you people are disgusting, depraved ghouls for profiting off of this man's death."

This week, Carson's friends told Gothamist that the slain activist would have empathized with his murderer. “I'm absolutely positive that he would immediately see that this was a person who was suffering from a lack of resources in our community," said state assemblywoman Emily Gallagher.

“I know he would have wanted people to use his death as a means to talk about structural wrongs in the city,” said Melissa Lozada-Oliva. We're guessing he'd probably be ok with the collective vacation fund too.

Russia lifted on Friday the ban on most of its diesel exports, two weeks after announcing export restrictions on diesel and gasoline to curb soaring domestic prices.

The Russian government said in a statement on Friday that as part of additional measures to keep the domestic fuel market stable, it is lifting the ban on exports of diesel delivered to seaports by pipeline, provided that the diesel producer supplies at least 50% of the diesel to the domestic market.

The ban on gasoline exports stays, for now.

As part of the measures announced on Friday, Russia also slapped very high export duties on fuel resellers to discourage companies that don’t produce the fuel themselves but buy it on the domestic market from exporting the fuels once the ban is lifted.

The government also restored in full subsidies to refineries to compensate them for the difference between fuel prices in Russia and outside Russia, with the intent to encourage refiners to sell fuel on the domestic market.

Two weeks ago, Russia surprised the markets by announcing a temporary ban on exports of gasoline and diesel to stabilize domestic fuel prices amid soaring crude prices and a weak Russian ruble. Diesel and gasoline exports were temporarily banned to all countries except for four former Soviet states� Belarus, Armenia, Kazakhstan, and Kyrgyzstan.

Since the EU embargo on imports of Russian fuel came into force in early February, Russia has diverted most of its diesel exports – previously going to the EU – to Turkey, the Middle East, North and West Africa, and Brazil in South America.

The ban affected those exports and analysts have said they don’t expect a prolonged ban on diesel shipments, because of Russia’s limited storage capacity which, once full, could force refiners to cut processing rates.

Just yesterday, Vladimir Putin’s spokesman Dmitry Peskov said that Russia would keep the ban on exports of diesel and gasoline “as long as needed” and no specific deadlines for lifting the export restrictions have been set.